Rocket Lab Stock Faces Scrutiny Ahead of Q1 Earnings

Analysts weigh potential earnings beat against a backdrop of high valuation and investment costs.

CANADA —

Key facts

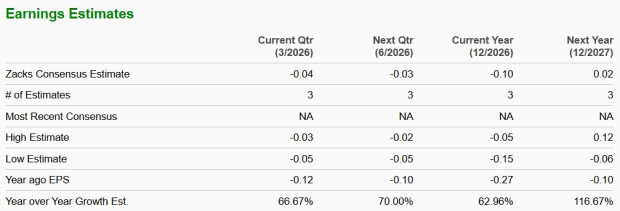

- Rocket Lab (RKLB) to report Q1 2026 results on May 7 after market close.

- First-quarter revenue forecast at $191.4 million, up 56.2% year-over-year.

- First-quarter earnings estimate projects a loss of 4 cents per share, a 66.7% year-over-year increase in losses.

- Rocket Lab's Earnings ESP is 0.00%, and Zacks Rank is #4 (Sell).

- Stock has risen 3.9% in the past three months, outperforming the industry's 6.9% decline.

- RKLB trades at a forward 12-month price-to-sales ratio of 46.09X, versus the industry average of 11.64X.

- Trailing 12-month return on invested capital (ROIC) is negative and lags the peer group average.

Rocket Lab Prepares for Q1 Earnings Amidst Valuation Concerns

Rocket Lab Corporation is poised to release its first-quarter 2026 financial results after the market closes on May 7. Analysts anticipate revenues to reach $191.4 million, a significant 56.2% increase from the same period last year. However, the earnings outlook presents a less optimistic picture, with the consensus estimate projecting a loss of 4 cents per share, marking a 66.7% year-over-year widening of losses. This earnings forecast comes as the company navigates a complex financial landscape. While revenue growth signals expansion, the projected increase in net losses raises questions about profitability. The market will be closely watching the company's ability to manage its expenses, particularly those associated with its ambitious Neutron program and ongoing research and development. The company's recent strategic acquisitions, including those of OSI and PCL, are expected to bolster its standing in defense, missile tracking, and space systems. These moves are intended to enhance Rocket Lab's vertically integrated capabilities and unlock new revenue streams. Yet, the associated operating costs and investments could continue to weigh on profit margins.

Mixed Earnings History and Predictive Indicators

Rocket Lab's performance against analyst expectations has been inconsistent in recent quarters. Over the past four earnings reports, the company has exceeded the Zacks Consensus Estimate only once, missing it on three occasions. The average earnings surprise during this period stood at a modest 4.29%. For the upcoming first-quarter report, predictive models do not strongly indicate an earnings beat. A key factor is the company's Earnings ESP (Expected Surprise Prediction), which stands at 0.00%. This metric, combined with the Zacks Rank, is typically used to gauge the likelihood of an earnings surprise. Rocket Lab currently holds a Zacks Rank of #4, categorized as a Sell. This combination of a neutral Earnings ESP and a low Zacks Rank suggests that the conditions are not favorable for an earnings beat this time around. Investors will be scrutinizing the management's commentary for insights into the factors driving these projections and the path forward.

Valuation Outpaces Industry Peers

Despite the mixed earnings outlook, Rocket Lab's stock has demonstrated resilience in recent months. Over the past three months, the share price has climbed 3.9%, a notable performance when contrasted with the broader industry's decline of 6.9% during the same period. However, this stock performance has propelled Rocket Lab to a significant valuation premium relative to its industry peers. The company's forward 12-month price-to-sales ratio is currently 46.09X, a stark contrast to the industry average of 11.64X. This suggests that investors are pricing in substantial future growth. Further complicating the valuation picture is the company's return on invested capital. Rocket Lab's trailing 12-month ROIC is not only below the average return of its peer group but also registers as a negative figure. This indicates that the company's investments are currently not generating sufficient returns to cover their associated costs, raising concerns about capital efficiency.

Strategic Acquisitions and Investment Pressures

The recent acquisitions of OSI and PCL are seen as pivotal moves designed to fortify Rocket Lab's position within the defense and space sectors. These strategic integrations are anticipated to unlock greater opportunities in defense contracts, missile tracking initiatives, and the development of sophisticated space systems. Specifically, OSI is expected to enhance the company's access to defense-related contract opportunities. Concurrently, PCL's integration is projected to streamline and potentially accelerate the production of both the Electron and Neutron launch vehicles. These acquisitions collectively aim to deepen Rocket Lab's vertically integrated operational model. Yet, the pursuit of these strategic goals is not without its financial implications. Significant investments in the Neutron program, coupled with increased research and development expenditures, are likely exerting pressure on operating margins. This sustained investment in future growth could limit the extent of overall earnings expansion in the near term.

TransDigm Group's Strong Performance Offers Contrast

In a separate financial report, TransDigm Group Inc. (TDG) has showcased robust performance in its recent fiscal quarters, offering a point of contrast to the challenges faced by Rocket Lab. first-quarter fiscal 2026 adjusted earnings of $5.80 per share, surpassing the Zacks Consensus Estimate of $5.48 by 5.9%. This figure also represented a 17.2% improvement from the $4.95 earned in the year-ago quarter. Total sales reached $1.56 billion, exceeding the consensus estimate of $1.51 billion by 3.3% and marking a 7.6% increase year-over-year. Furthermore, TransDigm's second-quarter fiscal 2026 results were equally impressive. Adjusted earnings per share came in at $9.85, topping the Zacks Consensus Estimate of $9.32 by 5.7% and growing 8% from the prior year. Sales for the quarter were $2.54 billion, up 18% from the previous year and exceeding the consensus estimate by 4.9%. This strong performance highlights a different trajectory within the aerospace and defense sector.

The bottom line

- Rocket Lab is forecasting significant revenue growth for Q1 2026 but expects a wider net loss.

- The company's earnings performance has been inconsistent, with a neutral earnings prediction model for the upcoming report.

- RKLB stock has outperformed the industry recently but trades at a high valuation multiple.

- Negative return on invested capital suggests current investments are not yielding sufficient returns.

- Strategic acquisitions aim to boost defense and space system capabilities but increase operating expenses.

- TransDigm Group's recent strong financial results provide a contrasting performance within the sector.

Buffalo Sabres Face Montreal Canadiens in Playoff Rematch

Victor Wembanyama Sets Playoff Blocks Record with 12 in Game 1, Spurs Lose

Manitoba Moose Goaltender DiVincentiis Stops 39 Shots in Playoff Shutout of Grand Rapids