Home Values Fall for Over Half of U.S. Owners as Market Defies Bubble Fears

Economists say the housing market is not in a bubble despite record prices and overvaluation in the Midwest and Northeast.

UNITED STATES —

Key facts

- Over half of U.S. homeowners have seen home values fall since last year, highest share in 13 years, per Zillow.

- Median existing-home sales price hit $415,200 in September, a record for that month, per NAR.

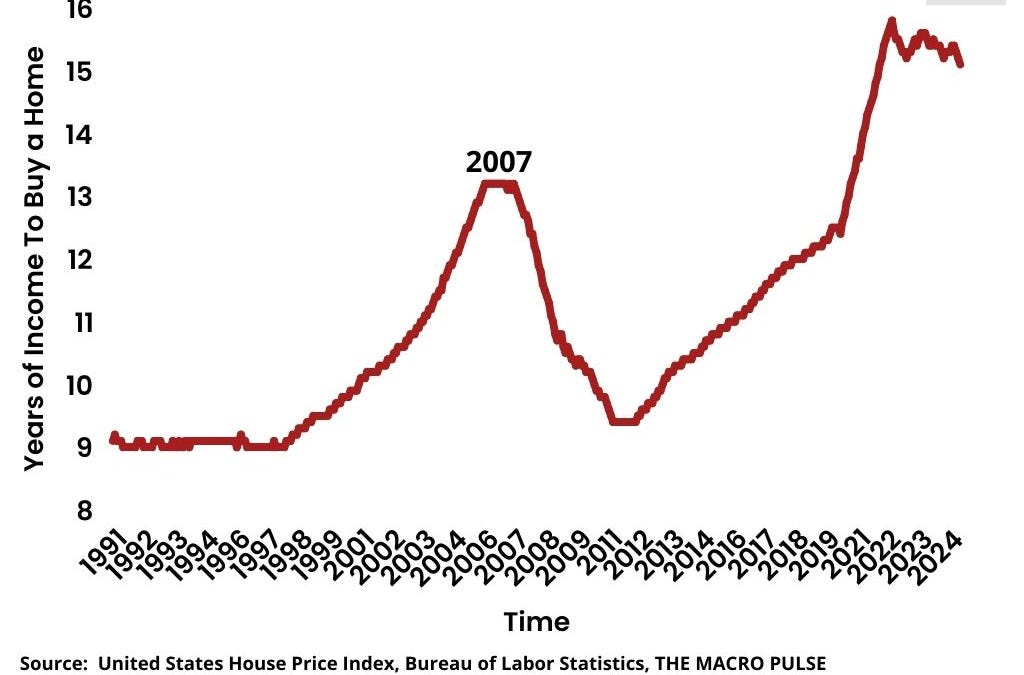

- Price-to-wage ratio reached 15 years of median income, exceeding the 13-year peak of the 2000s bubble.

- Mortgage rates remain high, locking in homeowners with 3% rates and suppressing sales.

- Homes are overvalued in the Midwest and Northeast, while other regions see sharp declines.

- Ken Johnson, University of Mississippi professor, says 'the party's over' but no crash expected.

- Richard Moody, Regions Financial Corp. chief economist, notes difficulty in generalizing about housing.

A Market of Contradictions

More than half of American homeowners have watched their property values decline over the past year, the highest proportion in 13 years, according to data from Zillow. Yet the median sales price of an existing home rose to $415,200 in September, the highest figure ever recorded for that month, the National Association of Realtors reports. Home sales remain largely depressed, caught between high interest rates that impede both buying and construction, a lock-in effect that keeps homeowners clinging to their 3% mortgage rates, and sellers who would rather delist than cut asking prices. The result is a market that appears simultaneously overvalued and underperforming.

Why Economists Dismiss a Bubble

Housing bubbles typically form when prices surge on a wave of speculation and high demand, then pop as demand collapses and supply floods the market, sending prices into a steep decline. Homeowners are left with negative equity and face potential foreclosure. But economists argue the current environment does not fit that pattern. 'Do I think the party's over? Yes,' said Ken Johnson, a professor of finance and real estate at the University of Mississippi. 'I just don't think we're going to have a crash.' The key difference, he and others note, is that today's high prices are not driven by speculative froth but by structural factors such as limited supply and elevated construction costs.

Overvaluation in the Midwest and Northeast

While the national picture is mixed, homes are clearly overvalued in parts of the Midwest and Northeast. In those regions, price-to-wage and price-to-rent ratios have stretched well beyond historical norms. Nationally, the price-to-wage ratio now stands at 15 years of median income, surpassing even the peak of the 2000s housing bubble, when it reached about 13 years. Yet housing is hyperlocal, meaning conditions vary sharply from one market to the next. Some areas are seeing steep price declines due to a high number of listings, while others remain overheated. 'It's really hard with housing to make generalized statements,' said Richard Moody, chief economist at Regions Financial Corp.

The Lock-In Effect and Stalled Sales

A persistent lock-in effect has frozen the market: homeowners who secured mortgages at historically low rates — often around 3% — are reluctant to sell and take on a new loan at current rates above 6%. This has suppressed inventory and kept prices artificially high in some areas. Sellers, meanwhile, are unwilling to drop their asking prices, preferring to delist their homes rather than accept a loss. The combination has created a standoff between buyers and sellers, with transaction volumes at multiyear lows. 'It wasn't too long ago when the big discussion was about when housing was in a recession,' Moody said. 'Now it's about if housing is in a bubble.'

What the Data Reveals About Affordability

The price-to-rent ratio has also widened, signaling that buying a home is increasingly unaffordable relative to renting. When it takes 15 years of median income to purchase a median-priced home, history suggests a correction is likely, economists warn. The yield curve, measured by the spread between 10-year and 2-year Treasury notes, has inverted, a classic recession signal that could further dampen housing demand. Inflation, exacerbated by tariff policies under the Trump administration, has eroded purchasing power. Mortgage rates have rocketed, making monthly payments unaffordable for many first-time buyers. The combination of high prices, high rates, and high inflation has pushed affordability to its worst level in decades.

Outlook: A Slow Adjustment, Not a Crash

Most economists expect a gradual cooling rather than a sudden collapse. Home prices may stagnate or decline modestly in overvalued markets, but a repeat of the 2008 crash is unlikely given tighter lending standards and a stronger labor market. 'I just don't think we're going to have a crash,' Johnson reiterated. Still, the risks are real. If the economy enters a recession, unemployment could rise, forcing more homeowners to sell and potentially triggering a sharper downturn. For now, the market remains in a state of uneasy equilibrium, with buyers waiting for prices to fall and sellers refusing to budge.

The bottom line

- Over half of homeowners have seen values fall, but economists say this is not a bubble, citing structural factors over speculation.

- Median home prices hit a record $415,200 in September, yet sales are depressed due to high rates and a lock-in effect.

- Price-to-wage ratio at 15 years exceeds the 2000s bubble peak, signaling severe overvaluation in some regions.

- Housing is hyperlocal: the Midwest and Northeast are overvalued, while other areas see sharp declines.

- A crash is unlikely, but a slow correction or stagnation is probable, with recession posing the main downside risk.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RN3K6DXILJGUHB7GMHHJCHZK2M.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/Z4E3VGL6ZFHFFCV7IYVHDWO674.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/OL66RXI6XFE2DJSYR4INVCEBNE.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/IP6XTBDAHVHMHKTXGFMSVYQ6QQ.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/K6P56KFG6BEYXGYMKVORXL53GE.jpg)

Spirit Airlines Faces Shutdown as Rescue Talks Collapse

S&P 500 Shatters 7,200 Barrier as Caterpillar and Alphabet Fuel April Rally

Mortgage Rates Jump to 6.45% as Iran Tensions Drive Bond Yields Higher