Atlassian Surges on AI-Powered Growth, Beating Estimates and Raising Guidance

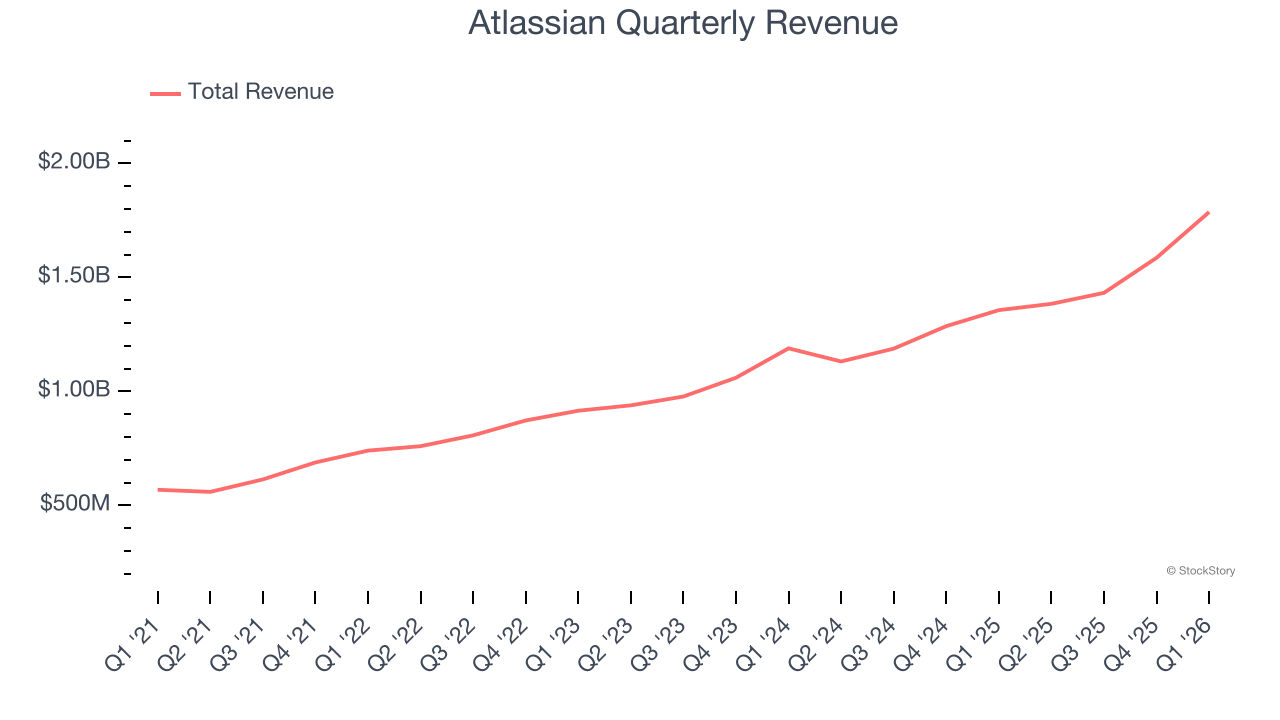

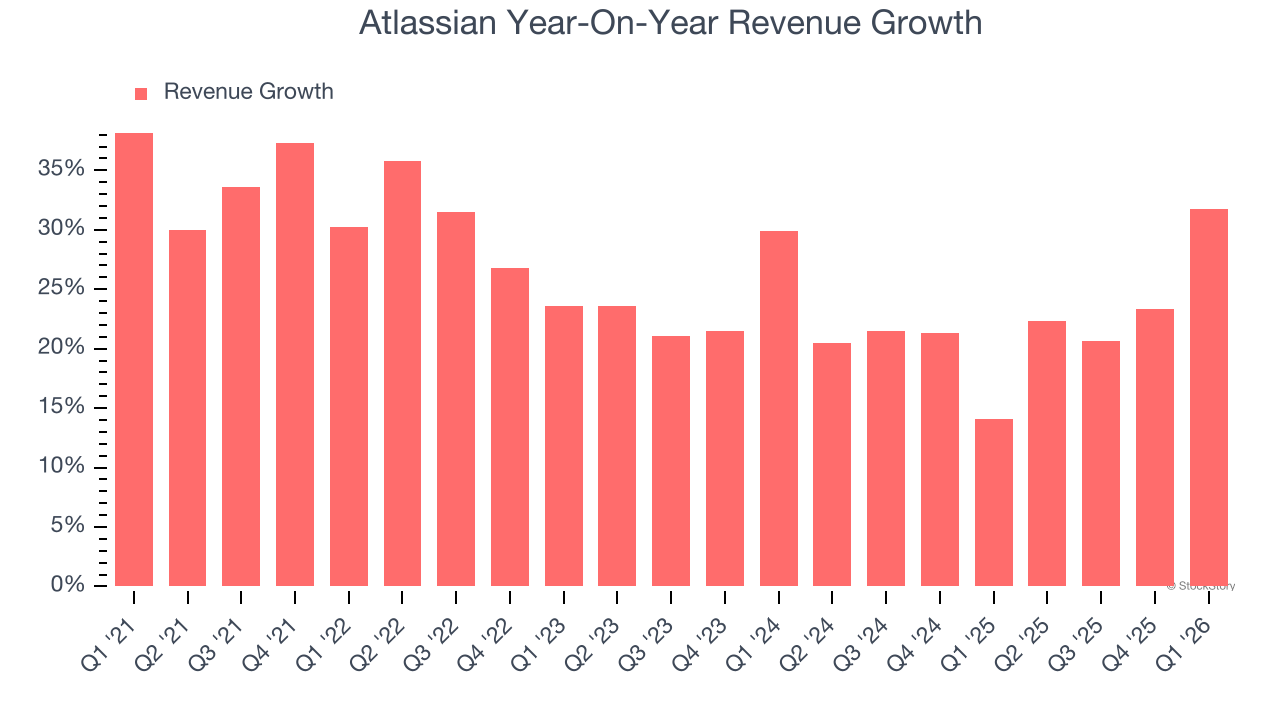

a 31.7% revenue jump to $1.79 billion, with profits far exceeding expectations, as customers commit to larger, longer-term deals.

UNITED STATES —

Key facts

- Revenue rose 31.7% year-on-year to $1.79 billion, beating analyst estimates of $1.7 billion.

- Adjusted EPS of $1.75 beat consensus by 31%.

- Adjusted operating income hit $607.2 million, a 28.5% beat vs. estimates.

- Full-year guidance raised across revenue growth, cloud revenue growth, and adjusted operating margin.

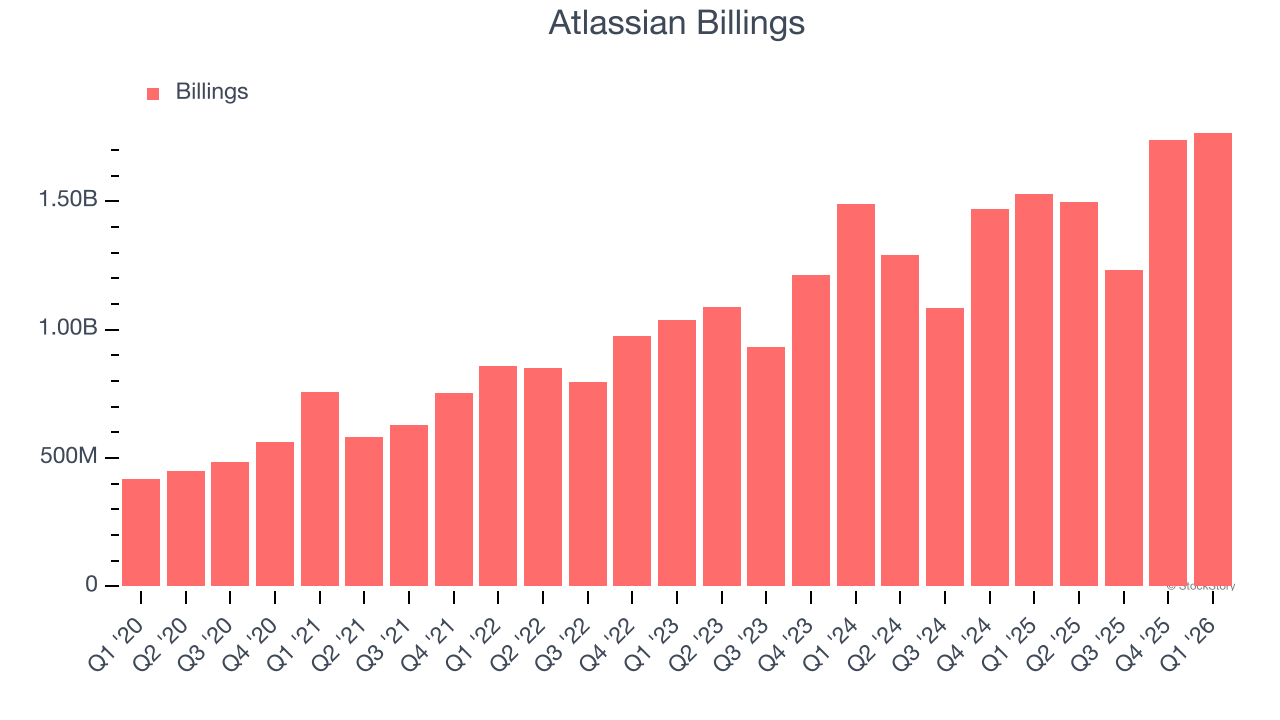

- Billings reached $1.77 billion, up 15.6% year-on-year.

- Free cash flow margin improved to 31.4% from 10.6% in the prior quarter.

- Operating margin fell to -3.1% from -0.9% a year ago.

- Market capitalization stands at $18.59 billion.

A Beat That Signals a Strategic Shift

Atlassian, the Australian-born collaboration software company, delivered a resounding first-quarter earnings beat for fiscal 2026, posting revenue of $1.79 billion — a 31.7% surge from a year earlier and 5.4% above analyst expectations. The company’s adjusted profit of $1.75 per share outpaced consensus by 31%, while adjusted operating income of $607.2 million came in 28.5% above estimates. The results, announced after market close, sent shares higher as investors digested a rare combination of top-line acceleration and margin expansion. Atlassian also raised its full-year guidance across all key metrics, including revenue growth, cloud revenue growth, and adjusted operating margin, signaling confidence in its strategic pivot toward larger, longer-term customer commitments.

Cloud and AI Fuel Customer Commitments

CEO and co-founder Mike Cannon-Brookes attributed the strong quarter to the company’s AI-powered platform, which he said is driving customers to “sign bigger, longer-term commitments” and connect their teams and workflows. The company’s cloud migration push, now augmented by generative AI features, appears to be accelerating deal sizes and contract durations. Billings, a key forward-looking indicator, rose 15.6% year-on-year to $1.77 billion, suggesting sustained demand. Free cash flow margin more than tripled sequentially to 31.4%, underscoring improved cash generation even as the company invests heavily in AI and cloud infrastructure.

Profitability Trade-Offs Emerge

Despite the headline beats, Atlassian’s operating margin turned negative, falling to -3.1% from -0.9% in the same quarter last year. The decline reflects elevated spending on sales, marketing, and product development as the company scales its AI capabilities and expands its go-to-market teams. Investors, however, appeared to look past the margin compression, focusing instead on the raised guidance and the accelerating revenue growth. The adjusted operating margin of 34% — well above the 28.5% beat — indicates that on a non-GAAP basis, the underlying business is becoming more efficient.

From Credit Cards to $18 Billion Market Cap

Atlassian’s journey from a startup funded by two Australian university friends using credit cards to a publicly traded company with an $18.59 billion market capitalization is a testament to its long-term sales performance. Over the past five years, the company has grown revenue at an annualized rate of 25.9%, outpacing the average software company and demonstrating sustained product-market fit. The company’s suite of tools — including Jira, Confluence, and Trello — has become essential for teams planning, tracking, collaborating, and sharing knowledge. The latest results suggest that the integration of AI into these products is deepening customer loyalty and expanding the addressable market.

Outlook: Raised Expectations and Execution Risks

For the next quarter, Atlassian expects revenue of approximately $1.66 billion, in line with analyst estimates. The raised full-year guidance implies confidence in continued momentum, but the company faces execution challenges as it balances growth investments with profitability targets. The competitive landscape in collaboration software remains intense, with rivals like Microsoft and Salesforce also embedding AI into their offerings. Atlassian’s ability to sustain its growth trajectory will depend on whether its AI features can deliver measurable productivity gains that justify premium pricing and long-term contracts.

The Verdict: A Pivot That’s Working

Atlassian’s Q1 results provide compelling evidence that its strategy of bundling AI with cloud migration is resonating with customers. The combination of a revenue beat, a profit surprise, and raised guidance is rare in the current enterprise software environment, where many companies are struggling to maintain growth amid macroeconomic uncertainty. Yet the negative operating margin and the need to continue heavy investment mean the path to sustained profitability remains uncertain. For now, the market is rewarding the company for its ambition, but the coming quarters will test whether Atlassian can convert its AI-led growth into durable, margin-accretive expansion.

The bottom line

- Atlassian’s Q1 CY2026 revenue grew 31.7% to $1.79 billion, beating estimates by 5.4%.

- Adjusted EPS of $1.75 exceeded consensus by 31%, and adjusted operating income beat by 28.5%.

- Full-year guidance was raised across revenue, cloud revenue, and adjusted operating margin.

- Billings rose 15.6% to $1.77 billion, and free cash flow margin improved to 31.4%.

- Operating margin turned negative at -3.1%, reflecting increased investment in AI and cloud.

- CEO Mike Cannon-Brookes credited AI-powered platform for driving larger, longer-term customer commitments.

Spirit Airlines Faces Shutdown as Rescue Talks Collapse

S&P 500 Closes Above 7,200 for First Time as Caterpillar and Alphabet Surge

Knicks obliterate Hawks 140-89 in historic 51-point playoff elimination