State Bank of India Posts Modest Q4 Profit Amid Treasury Headwinds

India's largest lender expects stable earnings despite lower investment income, with investors eyeing loan growth and dividend clarity.

INDIA —

Key facts

- State Bank of India announced Q4 FY26 results on May 8, 2026.

- Net profit for Q4 FY26 is projected to grow between 4% and 7% year-on-year.

- Net profit is estimated to reach ₹19,450 crore to ₹20,050 crore.

- Net interest income (NII) is expected to increase by 7% to 9% year-on-year.

- Net interest margin (NIM) is forecast to decline by 8 to 9 basis points to 2.7%.

- Gross NPA ratio is anticipated to improve to 1.5% from 1.6% quarter-on-quarter.

- A dividend for FY26 is under consideration by the bank's Central Board.

- SBI shares have delivered an 11.1% return to shareholders year-to-date.

Muted Earnings Growth Masks Resilient Core Operations

State Bank of India, India's largest public sector bank, is poised to announce its fourth-quarter financial results for fiscal year 2026, with analysts forecasting stable earnings despite pressures from diminished treasury income. The lender's performance is expected to be shaped by a delicate balance: while core banking operations show robust health, investment portfolio returns are likely to temper overall profit growth. This scenario sets the stage for a close examination of the bank's strategic navigation through a complex financial landscape. The bank's Central Board is scheduled to convene on May 8, 2026, in Mumbai to deliberate on the financial outcomes for the quarter and the full fiscal year ending March 31, 2026. A key agenda item will be the consideration of a dividend payout for FY26, a decision keenly awaited by shareholders. Following the announcement, an analyst meet is planned for later that evening, offering a platform for management to elaborate on the results and future outlook. Analysts project a modest year-on-year increase in net profit, potentially ranging between 4% and 7%. This growth, however, is expected to be significantly impacted by losses incurred in the bank's treasury operations, primarily due to rising bond yields. These headwinds are anticipated to offset gains from stable loan expansion, resilient margins, and a continuously improving asset quality, painting a picture of muted headline profit growth.

Treasury Losses Offset Stable Loan Growth and Margins

The State Bank of India's financial performance for the fourth quarter of FY26 is expected to be characterized by a divergence between its core lending business and its investment activities. While loan growth is anticipated to remain strong, propelled by demand across retail, SME, and corporate segments, the bank's treasury operations are likely to register losses. These losses stem from the impact of higher bond yields on the value of existing fixed-income securities, a common challenge in the current interest rate environment. Despite these treasury headwinds, analysts foresee stable operational performance. Loan growth is projected to be robust, with Motilal Oswal highlighting a credit growth guidance of 13–15% for FY26, supported by momentum in corporate, working capital, and emerging sectors such as data centres and green energy. This broad-based lending expansion is expected to provide a crucial cushion against the pressure from weaker treasury income. Furthermore, margins are expected to remain resilient, with net interest margins (NIMs) anticipated to hover around 3%. This stability is attributed to a favourable loan mix and stable funding costs, even as some analysts predict a slight decline of 8 to 9 basis points to 2.7% due to increased funding costs and a recent repo rate cut. Brokerages believe these steady margins are vital in supporting the bank's operational performance.

Asset Quality at Multi-Decade Lows, Dividend Under Review

A significant highlight of SBI's upcoming results is the continued strength in its asset quality. Market experts anticipate further improvement in the gross non-performing asset (GNPA) ratio, with estimates suggesting a decline to 1.5% from 1.6% in the previous quarter. The net non-performing asset (NNPA) ratio is expected to remain stable at a remarkably low 0.4%, reflecting a sustained period of clean-up and prudent risk management. These figures represent multi-decade lows for the bank, underscoring its success in controlling slippages and managing credit costs. Credit costs are likely to remain contained, indicating a normalization of the loan book rather than fresh stress emerging. This robust asset quality provides a strong foundation for future profitability and investor confidence. The bank's Central Board will also consider the declaration of a dividend for the fiscal year 2026. While details remain pending, this decision is a key point of interest for investors, who will be looking for a return on their investment alongside the bank's financial performance.

Financial Projections: Key Metrics and Estimates

According to various analyst estimates, State Bank of India's standalone net profit for the fourth quarter of FY26 is projected to fall within the ₹19,450 crore to ₹20,050 crore range. This represents a year-on-year growth of 4% to 7%, a notable moderation compared to the ₹18,643 crore profit recorded in Q4 FY25. Sequentially, net profit could remain flat, influenced by the aforementioned treasury income pressures, following a ₹21,028 crore profit in the preceding quarter. Net interest income (NII) is forecast to see a healthier increase, estimated between 7% and 9% year-on-year, reaching ₹46,150 crore to ₹46,950 crore. This growth is primarily driven by the expansion in the bank's loan book. For comparison, an NII of ₹42,775 crore in Q4 FY25 and ₹45,190 crore in the prior quarter. Provisions for the quarter are estimated at ₹4,580 crore, a decrease from ₹6,441 crore in the same period last year, and slightly higher than the ₹4,510 crore in the preceding quarter. These figures suggest a continued conservative approach to provisioning, aligning with the improving asset quality trends.

Investor Focus: Guidance on Rates, Deposits, and Growth

Beyond the headline numbers, investors will be keenly focused on the management's commentary regarding several key strategic areas. Guidance on deposit mobilization will be crucial, given the competitive pressures in the funding market and the bank's need to maintain a stable funding base. The outlook for loan growth across retail and corporate segments will also be a significant point of attention, particularly in light of the bank's upward revision of its FY26 loan growth guidance to 13–15%. The bank's strategy for navigating a lower interest rate environment will be a primary concern for the broader banking sector, and SBI's insights will be closely watched. Management's commentary on margins, credit costs, and the overall economic outlook, including factors like the West Asia crisis, global trade uncertainty, and commodity price volatility, will provide valuable context for future performance. Analysts will also be scrutinizing the bank's approach to managing its balance sheet in anticipation of potential market shifts. The bank's ability to sustain its growth trajectory while managing funding costs and interest rate sensitivity will be critical determinants of its long-term success.

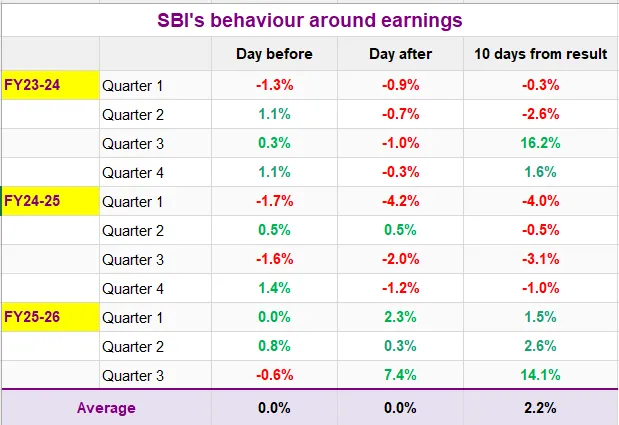

Market Performance and Trading Strategies

Ahead of the Q4 results announcement, State Bank of India's shares closed at ₹1,092, reflecting a slight 0.2% decline on the day. Despite this minor dip, the stock has demonstrated resilience, delivering an 11.1% return to its shareholders year-to-date. Technically, the stock is showing a positive structure, trading above its short-term moving averages, including the 20-day and 50-day exponential moving averages (EMAs). The immediate support level is identified near ₹1,060, a zone that has previously acted as a key demand area. The broader support remains around the 200-day EMA at ₹994. On the upside, ₹1,138 is the critical resistance level to monitor, with a decisive close above this point potentially signaling further upward momentum. For traders, the options data for the May 26 expiry suggests a potential price movement of approximately ±5.7%. This has led to discussions around strategies such as Long Straddles for those expecting significant volatility, or Short Straddles for those anticipating a period of lower price fluctuation. These strategies offer opportunities based on different market outlooks surrounding the earnings announcement.

The bottom line

- State Bank of India's Q4 FY26 net profit is expected to show modest year-on-year growth, constrained by treasury losses.

- Core banking operations, including loan growth and asset quality, remain robust and are key strengths for the bank.

- Net interest margins are projected to remain stable, though a slight decline is anticipated due to funding cost pressures.

- Asset quality continues to improve, with GNPA and NNPA ratios at multi-decade lows.

- Investors will closely monitor management guidance on interest rates, deposit mobilization, and future loan growth prospects.

- The bank's Central Board will consider a dividend payout for the fiscal year 2026.

Gujarat Board to Release SSC Results at 8 AM Today; Over 15 Lakh Students Await Scores

Bhuvneshwar Kumar Reaches IPL Milestone, Hailed as Elite Fast Bowler

Punjab Kings Remain Top Despite Back-to-Back Losses, Says Captain Shreyas Iyer After Narrow Defeat to Gujarat Titans